1. Introduction

A fundamental shift in the way capital is being allocated within global markets is currently taking place. The triple threats of climate change, environmental degradation, and social inequalities – together with the impacts of the COVID-19 pandemic highlight the need for new financing mechanisms to ensure a sustainable future. The awareness of these threats by the financial sector has led to the development of a sustainable finance market to directly address these challenges at scale.

Since the first green bonds were issued by the European Investment Bank and the World Bank in 2007, the sustainable debt market has grown exponentially. The market now involves debt issued by over 67 economies and multiple supranational institutions, and it incorporates a variety of public and private sector participants. The global green bond market reached a milestone of USD 1.9 trillion in issuance in December 2023, representing an estimated growth rate of 95% per annum [3].

The sustainable debt market has historically been dominated by green bonds, but the pandemic has catalyzed the next generation of social- and sustainability-labeled instruments to fund a broader range of environmental and social benefits. This paper provides a national update on the green, social, sustainable, sustainability-linked, and transition bond market, with a particular focus on local currency (LCY) sustainable bond markets in Vietnam. The first section outlines recent national initiatives, approaches, and policy developments to promote local currency (LCY) sustainable finance. And it concludes with recommendations and possible next steps for Vietnam to further advance sustainable LCY bond market development in the region.

2. Policies and approaches to promote local currency sustainable finance in Vietnam

The Vietnamese bond market grew to a size of more than USD0.8 billion in 2023. Over 80% of the volume coming from government debt, with development banks being the second-largest issuer type. In 2017, the Government of Viet Nam issued Decision No.1191/QD-TTg approving the Bond Market Development Roadmap, 2017-2020, with a vision that extends until 2030 [16].

The roadmap sets out goals to improve the domestic bond market so that it increases in size to about 45% of GDP by 2020 and 65% of GDP by 2030; and it focuses on measures to improve market depth and liquidity, in particular: Size of market is 0.8 billion USD, 6 issuers, 6 instruments, Average size of instrument is 0.2 billion USD, 2 currencies, Average tenor is 7.5 years [13].

2.1. Green bonds for long-term financing

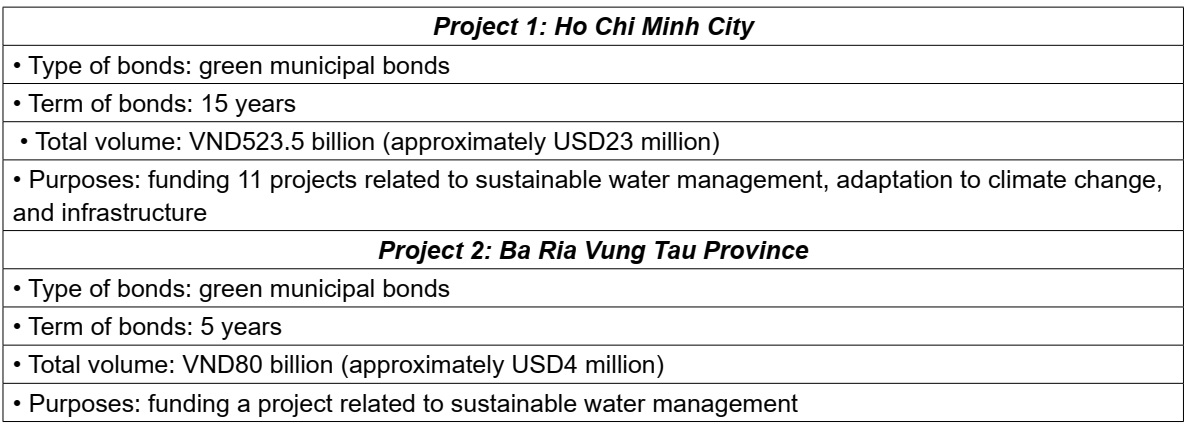

In 2016, the Ministry of Finance, partnered with the German International Cooperation Agency on a pilot program to issue green bonds in Ho Chi Minh city and Ba Ria Vung Tau province (Table 1) [13].

Table 1. Pilot green bond issuance programs in Vietnam:

The Vietnam Green Growth Strategy, 2011-2020 envisaged capital markets playing a key role in achieving the country’s climate goals by 2050 [10]. This has served as a basis for green finance to grow in Viet Nam. In 2017, the government approved the road map for bond market development, alongside mechanisms and policies for the green bond market, enabling issuers to raise capital for implementing green projects through the issuance of bonds [8].

In 2020, the government released Decree 153/2020/ND-CP regarding the private placement of corporate bonds and trading of privately placed corporate bonds in the domestic market, and the offering of corporate bonds in the international market.12 This decree serves as a guideline for the placement and trading of both conventional and green bonds in the onshore and offshore markets. Some notation points under the decree include: the definition and overview of corporate green bonds; principles for issuance of corporate green bonds; disclosing and reporting regimes for corporate green bonds; and issuance methods, redemption, and swaps of corporate green bonds.

Due to the lack of an appropriate legal framework to support issuance, no corporate green bond issuances have taken place in Vietnam to date. With the introduction of Decree No. 153, and the ongoing development of the Vietnamese financial markets, corporate green bonds are expected to be issued soon, with:

– Number of issuances by Green by the period of 2019-2023, respectively: 1 (2019), 2 (2020), 1 (2021), 1 (2022), 2 (2023). Number of issuances by Sustainability by the period of 2019-2023 is 0. Number of issuances by Social by the period of 2019-2023 is 0. Number of issuances by Social- COVID-19 by the period of 2019-2023 is 0. Number of issuances by Sustainability-linked bond by the period of 2019-2023 is 0. Number of issuances by Transition by the period of 2019-2023 is 0. [1]

– Cumulative issuance value by Green is 793.86 USD (well-proportioned 100%). Cumulative issuance value by Sustainability, Social, Social- COVID-19, Sustainability-linked bond, and Transition is 0 USD. [4]

2.2. Green Index

The Ministry of Finance issued Circular No. 155 on Disclosure of Information on the Securities Market in 2015 to assist businesses in disclosing information about green finance activities [7]. The Green and Sustainable Index, which tracks the performance of the top 20 sustainable stocks in the VN100 (the top 100 listed companies on the Ho Chi Minh Stock Exchange), was piloted from January to July 2017 and launched on the Ho Chi Minh Stock Exchange in July 2017 [2].

2.3. Banks and Green Credits

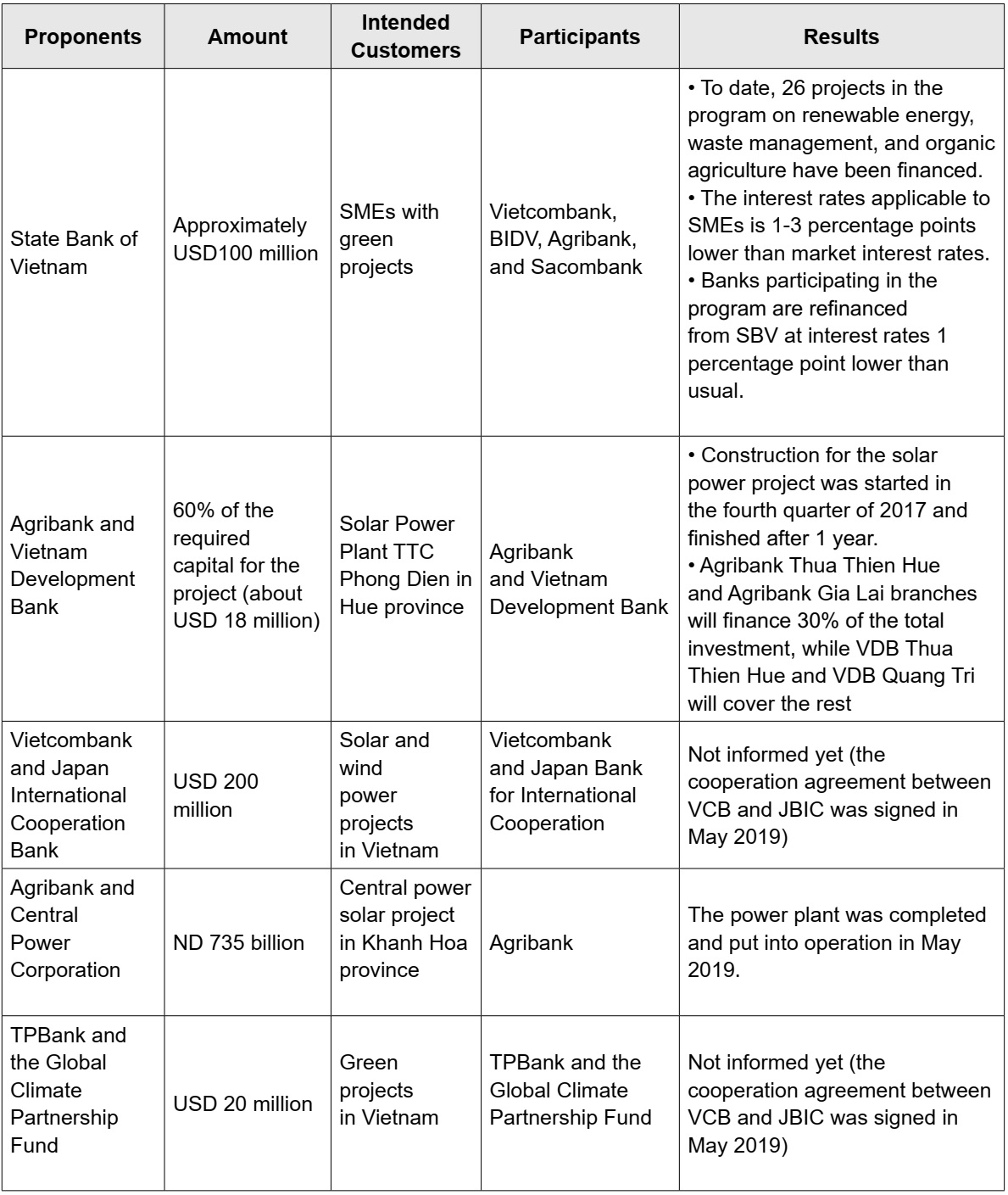

Vietnam is a bank-based economy, with the banking system financing approximately 70% of the economy’s capital needs [11]. As a result, the local banking system is a critical component of the country’s green financial market development. Indeed, the State Bank of Vietnam has been a vocal supporter of green economy campaigns. The State Bank of Vietnam issued Directive No. 03/CT-NHNN in 2015 to encourage green credit growth and to manage environmental and social risks in credit-granting activities [15]. Table 2 provides some examples of green credit programs in Vietnam.

Table 2. Green credit programs in Vietnam:

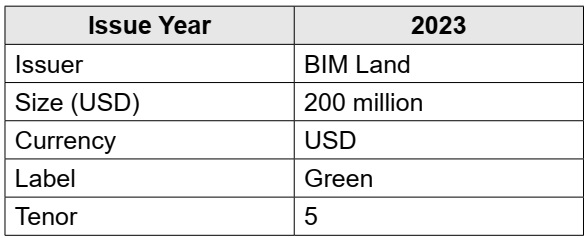

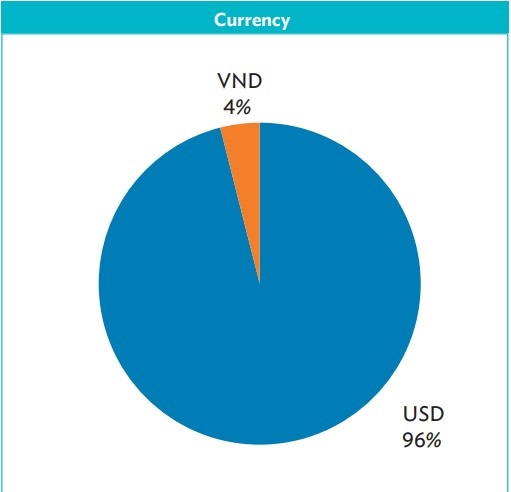

At the end of 2020, the National Assembly of Vietnam passed the new Environmental Protection Law, 2020 with major changes compared to the previous version. Among the changes are the inclusion of the definition, general requirements of green bonds, and potential incentives applicable to eligible issuers, which will be specified in the sub-law documents. A green taxonomy is being developed together with the promulgation of the law (table 3, table 4, chart 1):

Table 3. Policy Summaries for Vietnam:

Table 4. Largest Single Issuance:

Chart 1: Proportion of currencies in the market in 2023:

3. Conclusion and recommendations

To deliver on international climate and sustainability commitments, sustainable finance can serve a critical role – as a complement to public money – in channeling private investment into the transition to a low-carbon, resource efficient, climate-resilient, and inclusive economy.

Overall, Vietnam sustainable finance market continues to evolve in light of the pandemic and heightened attention on sustainability themes. Local currency capital market is at different stages of development in this country; the legal and policy frameworks vary, as does the extent of current sustainable finance market development.

The first recommendation below introduces several financial instruments to promote the development of the green bond market in Vietnam. Sustainable debt instruments are defined as instruments that have a label and directly finance sustainable projects or assets in the form of use-of-proceeds bonds and labeled loans. The green, sustainable, and social debt themes are based on the projects, assets, and activities financed.

– Green bonds: A green bond is commonly defined as a labeled fixed-income instrument where proceeds are specifically allocated for climate or other environmental projects. These are targeted typically (but not limited) to projects tackling energy efficiency, pollution prevention, sustainable agriculture, fishery and forestry management, protection of aquatic and terrestrial ecosystems, clean transportation, clean water, and sustainable water management, among others.

– Social and Sustainability Bonds: Drawing on existing market references and extensive research, the inclusion of social and sustainability bonds provides broad guidance on eligible sectors (and subsectors) that can be funded with social and sustainability bonds. Although work on a social taxonomy is underway in the European Union and elsewhere, neither a comprehensive taxonomy nor an equivalent classification and screening system for debt instruments aiming to achieve positive social or sustainable outcomes has yet been developed.

– Transition Bonds: Transition finance refers to instruments that are used to fund activities that are not low or zero-emission, but that play a short or long-term role in decarbonizing an activity or assisting an issuer in transitioning to compliance with the Paris Agreement. As a result, the transition label allows a wider range of sectors and activities to be included in the universe of sustainable finance. Transition bonds are currently derived primarily from polluting and difficult to abate industries. They do not fit any of the existing definitions of green bonds, but they are an essential part of the net-zero transition. Economic sectors include extractive industries such as mining, materials such as steel and cement, and other industries such as aviation.

– Sustainability – linked bonds: Performance or key performance indicators – linked debt instruments, more commonly known as sustainability-linked bonds or sustainability-linked loans, raise general-purpose finance and involve financial penalties if predefined, time-bound sustainability performance targets (e.g., greenhouse gas or carbon dioxide emission reductions) are not met. These penalties often either involve one or more of the following: coupon step-ups: an increase in the cost or amount of debt to be repaid (often from 10 to 75 basis points); premium payment: a self-imposed fine to be paid into an environmental, social, and governance (ESG) specific account; and offset purchase obligation: the mandatory purchase of carbon offsets (often used alongside one of the above penalties).

– Green loans: Green loans are any type of loan used to finance or refinance projects, assets, or activities that benefit the environment. Green loans are based on use-of-proceeds, with borrowing proceeds earmarked for eligible green assets in a transparent manner.

– Carbon-neutral bonds: A carbon-neutral bond is a debt-financing instrument that raises funds exclusively for green projects that reduce carbon emissions. Its primary objective is to direct funds to green, low-carbon, and cyclical sectors, as well as to assist markets and countries in achieving carbon-neutrality objectives.

– Blue bonds: Issuers may use the blue label if the funds are primarily used to support marine conservation and sustainable use of marine resources. Issuers must disclose information about the impact of relevant projects on the marine environment, the marine economy, and any other benefits to the climate. While it is important to note that not all blue bonds meet the green requirements (e.g., fisheries enforcement may require the use of fossil fuels).

– Poverty alleviation bonds: Poverty alleviation bonds, which have been introduced in the People’s Republic of China, are closely related to the goal of poverty eradication. “No Poverty” is the first of the 17 United Nations Sustainable Development Goals and is an important component of sustainable development globally. Poverty alleviation bonds have been used by government-backed entities, local governments, and corporate issuers to finance poverty alleviation and relocation.

– Rural Revitalization Bonds: Rural revitalization bonds, which have been introduced in the People’s Republic of China, refer to publicly or non-publicly listed bonds that raise funds for consolidating the results of poverty eradication, promoting the development of poverty eradicated areas, and carrying out comprehensive rural revitalization.

As a next step, the second recommendation below seek to promote the development of the green, sustainable, and social (GSS) bond market in Vietnam, taking into consideration the different levels of market development.

3.1. Supply Side

– Sovereign GSS bond issuances: Emerging market sovereign issuance can channel green capital flows where they are most needed.

– Unlabeled (climate-aligned) universe: These are investment opportunities that are not explicitly labeled as “green” by the issuer, but finance climate-aligned assets and activities.

– Advisory services for issuers: Both public- and private-sector advisory services can support new issuers with limited sustainable finance experience in determining the types of projects and assets that qualify as sustainable finance and address misperceptions that GSS bonds carry considerably higher costs. These services could be institutionalized through a partnership between the government and a development partner, or via a government agency that makes such services accessible.

– Grant schemes: Regulators and central banks can use grants to encourage sustainable finance flows.

– Green project pipelines: The growth of green infrastructure pipelines and associated green finance (including the green bond market) can be aided by key policy and institutional changes. International multilateral development agencies play a key role in blended finance, providing capital that mobilizes green or sustainable projects.

3.2. Demand Side

– Expand the investor base: Capitalize on increasing demand from institutional investors seeking sustainable investment opportunities.

– Central bank can help to “build back better”: Utilize the post-pandemic recovery toolkit used by central bank to protect country from future systemic risks – particularly climate related risks.

– GSS bond exchange-traded funds and indexes: Increase awareness and investor participation toward investing sustainably.

3.3. Ecosystem

– Mandates from government and regulators: Securities regulators, capital market authorities, and/or central bank that provide support mechanisms can encourage GSS bond issuance.

– GSS and sustainable finance platforms: Centralized information on green assets and projects should be made available in an easy-to-access portal or platform available in multiple languages.

Master. Duong Thi Thanh Tan – Department of Finance, Faculty of Economics and Business Administration, Vietnam National University of Forestry